Extending TCJA Would Provide a Modest Economic Boost, But at a High Cost

February 8, 2025

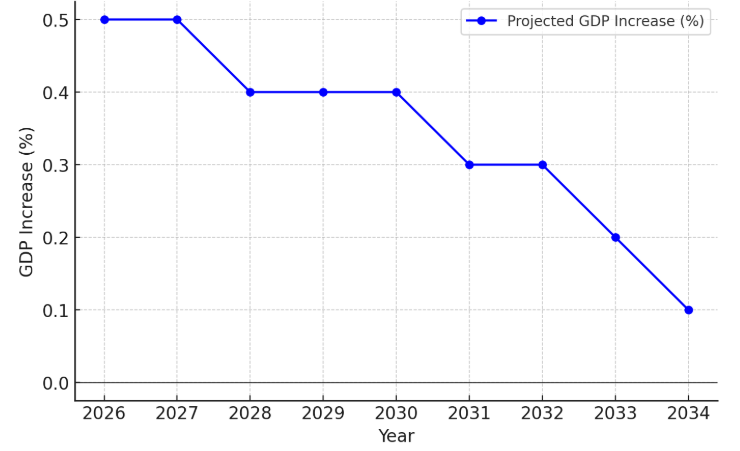

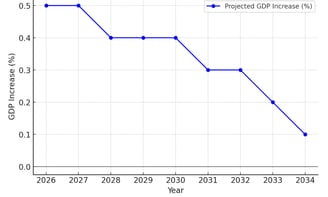

The American Institute for Tax Policy and Research (AITPR) estimates that extending the expiring provisions of the 2017 Tax Cuts and Jobs Act (TCJA) would result in a modest short-term economic boost. Between 2026 and 2034, gross domestic product (GDP) would rise by approximately 0.4% on average (see Figure 1). However, over time, these economic gains would be counterbalanced by growing federal deficits, which would limit business investment and slow long-term growth. Ultimately, the projected economic expansion would only offset about 6% of the estimated $4 trillion cost of extending the TCJA provisions.

Macroeconomic Impact of Extending TCJA Provisions

The Congressional Budget Office (CBO) and the Joint Committee on Taxation have conducted similar analyses, indicating that extending the TCJA’s individual tax cuts—including lower rates and adjustments to deductions and exemptions—would provide limited economic benefits. AITPR’s estimates also assume the continuation of key business tax provisions, such as full expensing for certain investments (bonus depreciation) and more favorable international tax rules. While these provisions would encourage short-term economic activity, they are insufficient to offset the long-term costs.

Short-Term Gains: Higher Incomes and Business Investments

AITPR projects that in 2026, overall taxes would be lower by more than 1% of GDP if TCJA provisions were extended. Lower tax rates translate into increased disposable income, leading to higher consumer spending. This, in turn, would stimulate business investment and hiring as companies seek to meet rising demand. Additionally, tax incentives for capital investment—such as full expensing—would reduce the cost of upgrading equipment and facilities, further encouraging economic activity.

Factors That Could Limit Economic Gains

Several structural factors would temper the economic boost from extending TCJA provisions:

Disproportionate Benefits for High-Income Households: Higher-income individuals tend to save, rather than spend, additional income. In contrast, lower-income households—who generally spend a larger portion of their earnings—may not benefit significantly from the extensions, as many already pay little to no federal income tax. Their tax relief would primarily come through refundable tax credits, which would not be received until 2027.

Federal Reserve Policy: The Federal Reserve may maintain higher interest rates to prevent the economy from overheating. Elevated borrowing costs for both businesses and households would discourage further investment and consumption, weakening economic growth.

Deficit-Funded Growth: AITPR’s projections indicate that while GDP would be higher by about 0.5% in 2026 and 2027 under a TCJA extension, these effects would fade over time due to rising interest rates, reduced private investment, and other macroeconomic adjustments.

Long-Term Tradeoffs: Lower Taxes vs. Rising Deficits

Extending TCJA provisions would lower workers’ marginal tax rates, making employment more financially rewarding and potentially increasing labor supply. Similarly, the tax cuts could encourage higher levels of saving, increasing capital available for investment. However, these benefits must be weighed against the negative impact of rising federal deficits.

The Cost of Deficits: A Long-Term Drag on Growth

While tax cuts generally promote work and saving, reduced federal revenue would lead to larger budget deficits and higher borrowing costs. Increased government borrowing would push up interest rates, which in turn would “crowd out” private investment. As deficits grow, this effect would become more pronounced, eventually diminishing economic gains.

Between 2028 and 2034, AITPR estimates that the combined effects of increased incentives to work and save, alongside rising deficits, would result in an average GDP increase of 0.4% (Figure 1). However, within 25 years, the cumulative effect of deficits would likely reduce economic output.

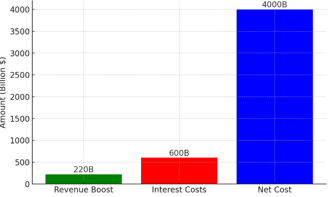

The Fiscal Impact: Offsetting Only a Fraction of the Cost

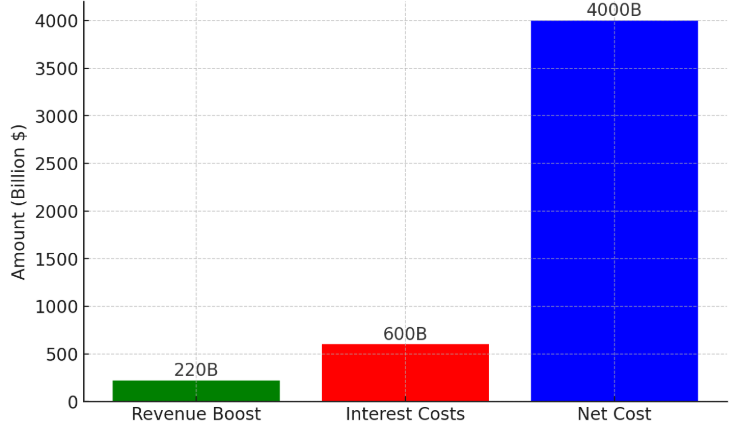

Over a ten-year period, economic growth from extending TCJA provisions would increase taxable incomes, generating an estimated $220 billion in additional revenue—covering just 6% of the $4 trillion cost of extension (Figure 2). By contrast, CBO projects that rising debt levels associated with the extension would increase federal interest costs by over $600 billion during the same timeframe. These interest costs are not included in the official $4 trillion cost estimate but represent a significant fiscal burden.

Figure 1: Projected GDP Increase Under TCJA Extension (2026-2034)

Policy Considerations: Balancing Growth and Fiscal Responsibility

Extending TCJA’s expiring tax provisions would provide a temporary boost to the economy, but at the cost of worsening the federal government’s already challenging long-term fiscal outlook. Policymakers must carefully weigh these tradeoffs when considering which provisions, if any, to extend. Thoughtful reform efforts should focus on maximizing economic benefits while mitigating long-term risks associated with rising debt.

For ongoing analysis of federal tax policy and its economic impact, visit AITPR’s website and stay connected with The Institute’s latest research.

Figure 2: Revenue Impact of TCJA Extension (2025-2034)

Tax Policy Insights Delivered